The Downturn That No One’s Talking About

A few of the recent headline subjects pushed out on the wire include “Wall Street is in a Bear Market”, “The Crypto Bear Market Could Last Two Years”, and “When Will the Nasdaq Bear Market End?”. None of these topics address the severe damage incurred within the average “Boomer” portfolio year-to-date by what one might normally think of as an unsuspecting menace: Bonds.

Bonds, otherwise known as Fixed Income, have been a mainstay of retail investor portfolio makeup over the past 100 years. Often touted as “risk-free”, the investor would traditionally receive a coupon payment each year, and the promise that their principal investment would be repaid on maturity. When the asset was a government bond, these promises are historically all but guaranteed as the government can simply print money to make the coupon payments, and print more money, if need be, to repay the principal on maturity.

Cracks begin to show as money printing becomes more egregious. First, investors pick up on the fact that when their bonds yield 2%, and inflation is at 5%, the “real” rate of return on their investment -3%. That’s before fees, and before taxes. Then, as governments around the world attempt to reel in soaring inflation caused by unprecedented spending throughout the pandemic, central banks have no choice but to raise interest rates.

Remember, there’s an inverse relationship between interest rates and the price of bonds. When interest rates go up, the price of bonds go down. Not only has the investor lost “real” purchasing power for the past several years, now the actual market value of their bonds has been hammered.

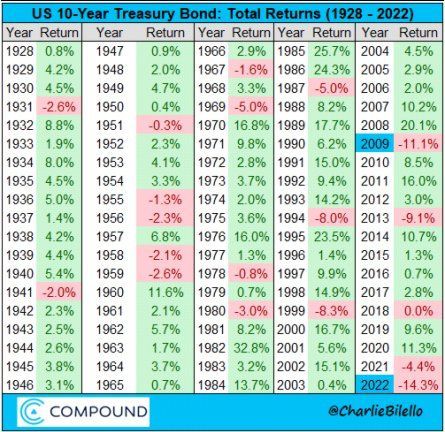

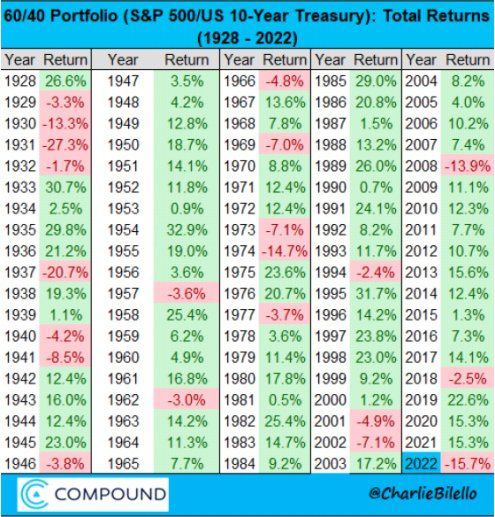

Looking at historical US 10-Year Treasury Bond total returns, 2022 is the worst year ever for bonds (data goes back to 1928). Reviewing the performance of a 60% Equity/40% Bonds portfolio (standard baby-boomer asset mix) you need to go back to 1937 before you will find a worse year than 2022.

How could some of this damage have been mitigated? First, by shortening the duration (term) of the fixed income component to the portfolio. The shorter the term of the bond, the less susceptible it is to change in interest rate. Second, by increasing the quality of the bonds themselves. All else being equal, high-quality bonds will perform better than their less credit-worthy cousins during times of turmoil. Third, by diversifying outside of the traditional 60/40 split. This might include a disciplined exposure to preferred shares, and alternative asset classes.

The key point here is that times are changing. The idea that bonds are a “safe” asset class is rightfully being called into question. The noteworthy challenge is how best to effectively structure a portfolio while considering one’s individual tolerance for risk, liquidity requirements, income tax considerations, compliance obligations, and of course return expectations.

Moving forward, retail investors may have to choose between a steady erosion of purchasing power from the bond side of their portfolio, or the increased volatility of marketable alternative assets.

About the Author: Taylor Amonson

Taylor comes to Unbiased Financial Services Inc. from the banking industry where he spent 3 years with RBC, leaving as Senior Account Manager. During his time with the Royal Bank he obtained his Certified Financial Planner (CFP) designation. His formal education includes a BA from the University of Victoria, which involved a one year exchange at the University of East Anglia. He also holds an MBA with Distinction from Edinburgh Business School, Heriot-Watt University.

SHARE THIS POST:

RECENT ARTICLES

Take Control of Your Wealth

Unbiased Financial Services offers personalized wealth management solutions tailored to your needs.

CONNECT WITH US ON LinkedIn

Stay connected with Unbiased Financial Services Inc. by following us on Linkedin. Get the latest updates, stories, & opportunities to get involved.

JOIN OUR NEWSLETTER

STAY IN TOUCH WITH THE LATEST EVENTS, NEWS & OFFERS

To join our mailing list, please insert your e-mail address below and click subscribe. Your information will not be sold or distributed to any unrelated third party companies.

Newsletter Subscription

Unbiased Financial Services: Your trusted partner in wealth management. Two decades of experience, personalized solutions, expert guidance for financial success.

QUICK HELP LINKS

CONTACT INFORMATION

Office: #5, 1204 3rd Street SE Calgary, Alberta T2G 2S9

Phone Number: (403) 671-1707

BUSINESS HOURS

- Mon - Fri

- -

- Sat - Sun

- Closed